The Market Is Sleeping on Rocket Doctor's 21 Million Covered Lives

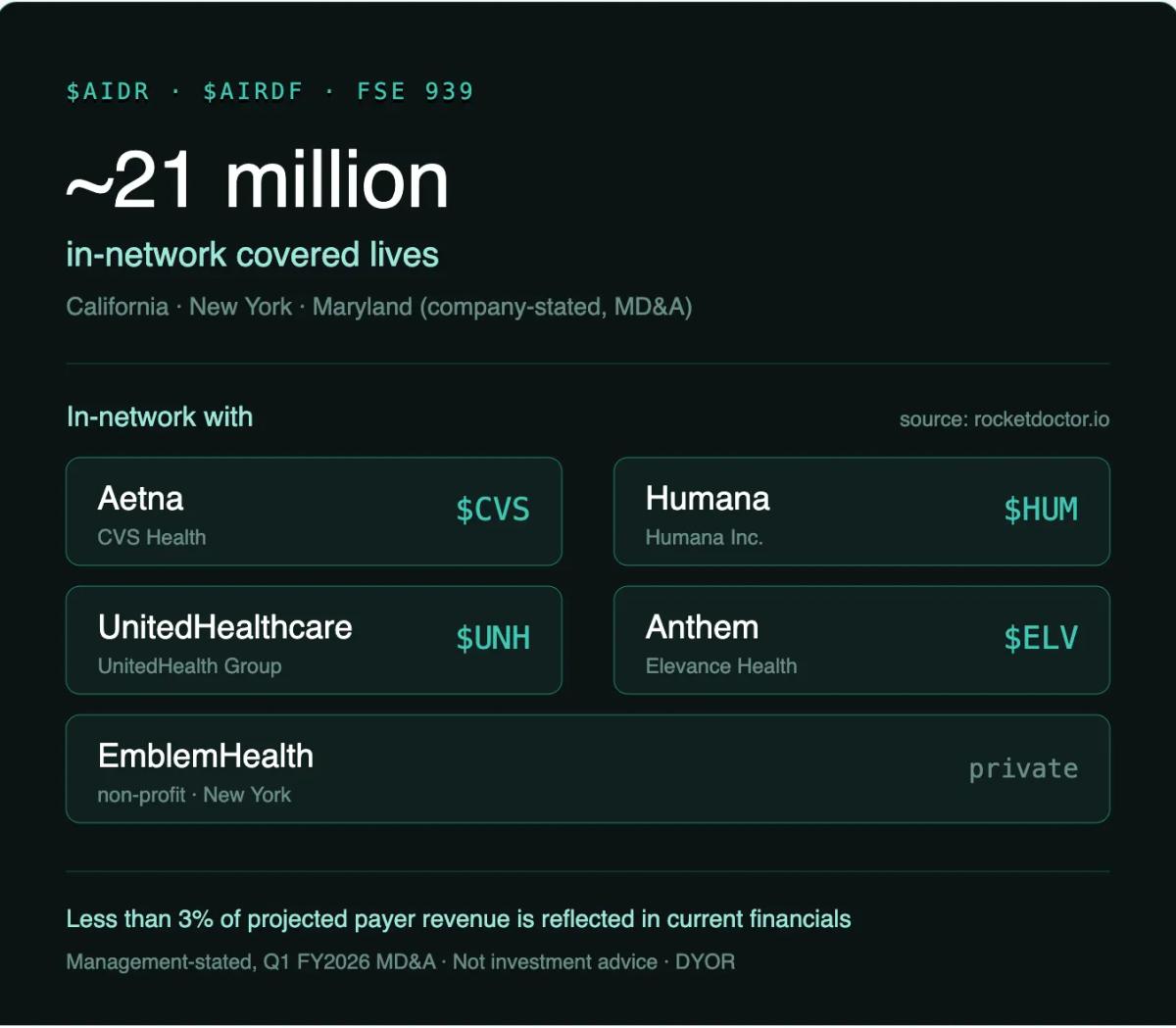

There’s a number sitting in Rocket Doctor’s latest MD&A that I think the market has badly underweighted: approximately 21 million in-network covered lives across California, New York, and Maryland. I want to be precise about what that figure is and isn’t, because the whole point of this thesis is to be right, not loud. So let me frame it the way I’d want a skeptic to frame it back to me.

There’s a number sitting in Rocket Doctor’s latest MD&A that I think the market has badly underweighted: approximately 21 million in-network covered lives across California, New York, and Maryland.

I want to be precise about what that figure is and isn’t, because the whole point of this thesis is to be right, not loud. So let me frame it the way I’d want a skeptic to frame it back to me.

What “21 million covered lives” actually means

This is a management-stated figure from the company’s Q1 FY2026 MD&A, not a revenue number, not a patient count, and not something you’ll find broken out line-by-line in the audited statements. It’s the size of the in-network, addressable population: people whose insurance plans Rocket Doctor’s credentialed physicians can now bill in-network in three states.

The state-level breakdown management provides:

- California ~8.1 million in-network members

- New York ~9.9 million beneficiaries with direct access

- Maryland ~3.1 million residents under state Medicaid and Medicare programs

That’s the ~21 million. It is an access footprint, not a revenue run-rate.

Why I think this is understated

Here’s the part that I keep coming back to. Management has stated that less than 3% of the projected revenue from these payer agreements is reflected in current financials.

Sit with that. The 21 million number is the denominator. The revenue actually showing up in the financials today represents only a sliver of what these in-network contracts are designed to produce once credentialing and patient volume catch up. The contracts exist. The access exists. What hasn’t happened yet is the conversion of credentialed doctors × in-network patients × completed, billable visits.

And the early conversion signal is moving in the right direction. In Q1 FY2026, U.S. monthly completed visits grew 283%, and that pace continued into April with a further ~69% month-over-month jump to roughly 1,200 completed visits. The binding constraint is provider supply; the company roughly doubled the number of active providers to ~80 by the end of May 2026 and is openly working on faster credentialing pathways.

So the bull framing isn’t “21 million people will use Rocket Doctor.” It’s narrower and more defensible: the access infrastructure is built, the revenue from it is almost entirely unrecognized, and the volume curve is bending the right way.

Who is actually in-network with Rocket Doctor

This is the part I think deserves more attention than it gets. When you go in-network with the largest payers in the U.S., you’re not just adding lives, you’re collecting credibility. These are the counterparties whose credentialing bars are notoriously hard to clear.

Rocket Doctor’s own website publicly lists the following insurers under “In-network with.” I’m sourcing this directly from rocketdoctor.io rather than the filings, because the MD&A describes most of these agreements generically (”another major insurer,” “a major national payer”) — the named roster comes from the company’s public-facing site, and only Aetna is named in the filings themselves. Worth flagging for anyone who wants to be rigorous.

The named payers, with public tickers where they apply:

- Aetna: a CVS Health company · CVS 0.45%↑

- Humana: HUM 1.58%↑

- UnitedHealthcare: UnitedHealth Group · UNH -0.12%↓

- Anthem: now Elevance Health · ELV 0.63%↑ (Anthem rebranded the parent to Elevance in 2022; the Anthem brand persists on plans)

- EmblemHealth: a New York non-profit · no ticker, privately held

Four of the five map to large-cap public insurers. When a CSE micro-cap is sitting in-network alongside $UNH, $CVS, $HUM, and $ELV, that’s a different kind of signal than a press release. Those companies don’t credential providers casually.

(One honest caveat: “in-network” is a plan-and-line-of-business-specific status. Being in-network with Aetna in New York is not the same as being in-network with every Aetna product nationwide. The logos are real and meaningful, but the footprint is the narrow credentialed one, not the payer’s entire national book.)

The risks I’m not pretending away

- Recognition lag is real. The U.S. model is largely cash-based for Medicare/Medicaid, with a 45–90-day collection lag. Revenue trails activity.

- Credentialing is the throttle. Visit volume can’t outrun the provider count. ~80 active providers is the current ceiling on how fast the 21M converts.

- Named ≠ filed. As above, most payer names are sourced from websites, not SEDAR filings. I flag it; I don’t bury it.

- Micro-cap reality. Thin float, financing risk, and the usual CSE liquidity dynamics apply.

- Geographic mismatch. The 21M lives are concentrated in three states. National “reach” narratives need to respect that the in-network footprint is state-specific.

Bottom line

The thing that changed the company’s profile this year isn’t a single contract — it’s that the in-network access footprint crossed into eight-figure covered-lives territory across three states, alongside the biggest names in U.S. health insurance, while <3% of the associated revenue is recognized.

I think the market is still pricing Rocket Doctor as a Canadian telehealth micro-cap. The 21 million covered lives, and who those lives sit with, say it’s becoming a U.S. payer-network story. The test, as always, will be the Q2/Q3 visit volume data. That’s the number that turns access into revenue.

Disclosure (repeated because it matters): I am long $ AIRDF/$AIDR, with over 1.2M shares. I am not a financial advisor, and this is not investment advice. Figures cited as “management-stated” come from company filings and commentary and have not been independently verified by me. Named insurers are sourced from rocketdoctor.io. Do your own research.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.